For years, I have seen many stock market bubbles form and then burst. Stock market experts seem to sing the same old tune. They are looking beyond present conditions toward what they believe will happen in the future. Bubbles usually form when there is too much optimism and tend to burst when the economic reality sets in.

The basic human suffering from Covid-19 gets more and more insane by the day. The reality on the ground is that the spread of Covid 19 is getting worse in the U.S. and other parts of the world, not better.

Why then have money managers continued to push stock prices higher?

- They believe that whatever is happening today doesn’t matter, but it is where we are going tomorrow that matters. In this case, tomorrow is 2021.

- Government stimulus measures seem to have lessened some investor fears. The CARES Act, the $2.2 trillion coronavirus relief package issued one-time stimulus payments to American households. It expanded unemployment benefits and created a forgivable loan program for small businesses.

- The Federal Reserve has also used aggressive measures to make sure businesses and municipalities can access ready cash.

- Investor optimism has been buoyed by phased state reopenings that have begun across the country and the expectation of a vaccine.

- There has been a rebound in consumer spending and some companies are rehiring.

- A survey of financial advisors suggests they’re taking a rosy view over the long term. A quarter of advisors expect to increase their stock recommendations to clients over the next year.

Here is a dose of reality

It turns out that much of the S&P 500 returns come from just 10 companies: Microsoft, Apple, Amazon, Google, Facebook, Visa, Mastercard, Nvidia, Netflix, and Adobe. As a group they are up 35% since the beginning of the year. As a group, the other 490 are down more than 10%.

Just three stocks make up more than a third of the Nasdaq 100 Index. I bet you can guess which three. Apple, Amazon and Microsoft together are now valued at nearly $5 trillion. That’s larger than the entire economy of Germany and nearly the size of the Japanese economy

In a true bull market, you see most stocks rising, often to new highs. A rising tide should lift nearly all boats. The percentage of NYSE stocks closing above their 200-day moving average is only 37% but it was near 70% in January.

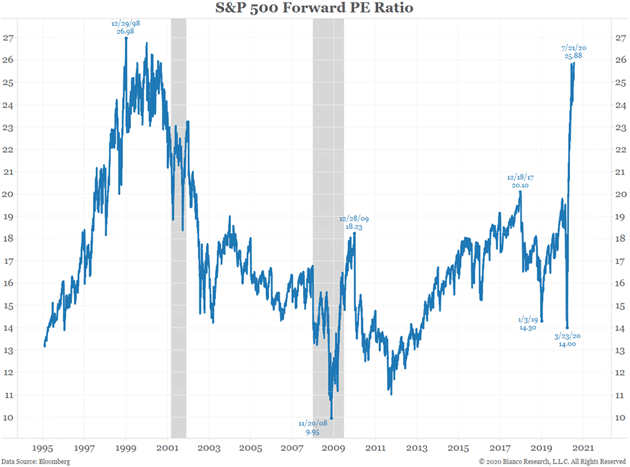

The market has already assumed that current earnings will be bad. Analyst earnings projections tend to overestimate even in good times and analysts tend to have a herd mentality, usually tracking one another. I found a chart by Jim Bianco to illustrate a possible valuation bubble.

The problem with stock market bubbles is you can never predict when they will burst. The most notable one was the dot com bubble that formed from 1995 to 2000 and burst in 2001. There are a few stocks today that are valued similar to some of the past dot com stocks.

Tesla is a perfect example, it has a market value of 262 billion based on sales revenue of 25 billion. You can also add Shopify to the bubble list that has a market value at 110 billion with only 1.7 billion in sales revenue.

Some economic reality may set in next week with the release of second quarter GDP on Thursday July 30. (Analysts are expecting a decline of 33%), along with Friday’s release of consumer spending, Chicago’s purchasing managers index (PMI) and consumer sentiment index.